Our Results

Although it is difficult to quantify the benefits obtained by our clients thanks to our tax advice, the numerous favorable decisions in tax disputes are, on the other hand, much more objective.

Maître Nicolas Rozenbaum has a perfect command of the tax procedure and is able to assist you during all phases relating to a tax audit (proposal for rectification, taxpayer observations, hierarchical appeals, departmental tax commission and fees). on turnover,...).

The firm handles all types of tax disputes in personal and corporate taxation throughout France.

Here are some examples of the type of litigation that the NR lawyers firm has handled:

Tax audit relating to the acquisition of a historic monument

A customer was the subject of atax audit relating to the acquisition of amonument having followed up on a proposal for rectification for a significant amount.

Maître Nicolas Rozenbaum "took advantage" of the receipt of this rectification proposal to be able to make a complaint relating to another type of dispute (the receipt of a rectification proposal in fact making it possible to reopen aclaim deadlinewhich would have expired in the absence of receipt of a rectification proposal).

This more than offset the amount initially claimed by the tax authorities as the tax authorities were forced to provide relief of €65,746.

Vaccounting verification

A customer was the subject of aaccounting audit. After analyzing the rectification proposal, Maître Nicolas Rozenbaum noticed an error in the calculation of the rectifications linked to VAT. The tax administration immediately recognized its error, which led to aimmediate relief of €144,000 taking into account late payment interest and surcharges.

Amount of VAT claimed by the administration in its rectification proposal:

Amount of VAT claimed by the administration following the observations of Maître Rozenbaum:

Vaccounting verificationAndVAT adjustment

A client, a construction company, was the subject of aaccounting auditand a VAT adjustment. Maître Nicolas Rozenbaum invoked article 283-2 nonies of the General Tax Code requiring self-liquidation of VAT in the event of subcontracting.

This resulted in a total abandonment of rectifications for a year.

Raddress in matters of property tax

In the context of another case, an SCI was the subject of an adjustment in terms of property tax. Maître Rozenbaum was able to obtain relief of €3,278 for one year. Maître Rozenbaum then took advantage of this relief to make a claim for the following years to the extent that the amount of the property taxes depended in part on the amount of the property tax for the year having benefited from arelief.This resulted in an additional relief of €6,166.

Tfocus on vacant housing of aSCI

In another case, Maître Rozenbaum was able to obtain relief of €6,359 excluding late payment interest under thetax on vacant housing of aSCI.

Dispute of rerection

A client received an amended property tax notice for more than €10,000 in respect of his agricultural land which the tax administration taxed according to the rules for professional premises ("open-air storage location") on the grounds that this client stored bo Master Rozenbaum. This adjustment also led to a property tax increase of €3,000 per year.

Maître Rozenbaum contacted the tax conciliator to contest this adjustment. The conciliator completely canceled the disputed tax.

Accounting audit

An SARL carrying out the driving school activity was the subject of an accounting audit leading to a reconstitution of revenue.

The tax administration considered that the SARL's accounting had no probative value. This tax audit resulted in the sending of a rectification proposal relating to an increase in corporate tax, VAT, and income deemed distributed, all subject to increases for deliberate failure, i.e. a total claimed by the tax administration of more than €120,000.

Following the observations of Maître Rozenbaum and the referral to the regional contact within the framework of a hierarchical appeal, the tax administration abandoned all of the duty reminders (except €1,189 of VAT).

Property tax relief

Following a complaint, Maître Nicolas Rozenbaum was able to obtain a reduction of €11,000 in property tax for a client.

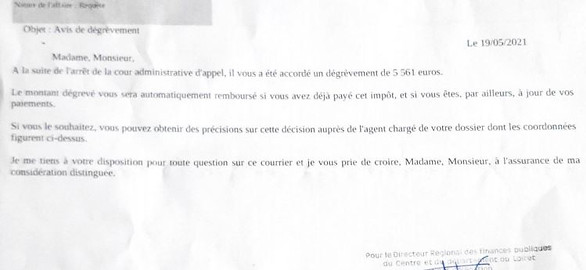

Transfer of temporary usufruct of SCI shares

Relief of nearly €200,000 following the decision of an administrative court of appeal in the context of the transfer of temporary usufruct of SCI shares